On 9 April 2020, I posted a webinar on this topic. My purpose was to walk viewers through Article 3b of the Cross Border Payment Regulation and state when it applies and when it doesn’t, depending on the funds flow of the firm. Since this webinar was posted, the UK’s transition period with the EU has ended and the Cross Border Payment Regulation has been “onshored” (i.e. been made part of UK law).

Whilst there were some changes made by the UK Government to the Cross Border Payment Regulation when it was “onshored” (for example, PSPs will no longer have to comply with the equality of charges requirements), the requirements on transparency on currency conversion charges under Article 3a and Article 3b (the content of this blog and the webinar) have been preserved.

It is worth noting, that whilst this “onshored” regulation might not require your UK PSP to be transparent on your currency conversion charges, the Financial Conduct Authority may still require UK PSPs to be transparent as part of their obligation to treat customers fairly.

Please don’t treat this blog as legal advice. It is intended as general information. If you would like specific legal advice for your PSP, please don’t hesitate to contact us.

When does Article 3b of the Cross Border Payment Regulation apply?

Article 3b applies if three conditions are met:

- you are offering national or cross-border credit transfer within the EU;

- those credit transfers are in euros or the currency of another member state; and

- you carry out a currency conversion in relation to that credit transfer.

Rather than cover all possible scenarios, I describe three examples used by my clients in which Article 3b may or may not apply.

What is a credit transfer?

Before examining each model in turn, I clarify what a credit transfer is, since this is the method of payment under consideration. A credit transfer is when a client sends a payment instruction to its payment institution or payment service provider (PSP) to transfer money from its payment account to the payment account of another person. The PSP then sends the money from the client’s payment account with the PSP to the beneficiary’s payment account.

Please note that references to payment accounts include electronic money accounts.

Model A

The first model I examine is the money remittance model.

While there is a foreign exchange transaction here, there is no payment account and therefore no credit transfer. Accordingly, Article 3b does not apply to this money remittance model.

Model B

I then examine a model where payment accounts are used.

The transfer of money from the client’s payment account in the sale currency to the beneficiary’s payment account in the purchase currency is, in our view, a credit transfer. In between money leaving the client’s payment account and arriving in the beneficiary’s payment account, a foreign exchange transaction has been executed. Accordingly, there has been a foreign exchange transaction in relation to the credit transfer and Article 3b does apply.

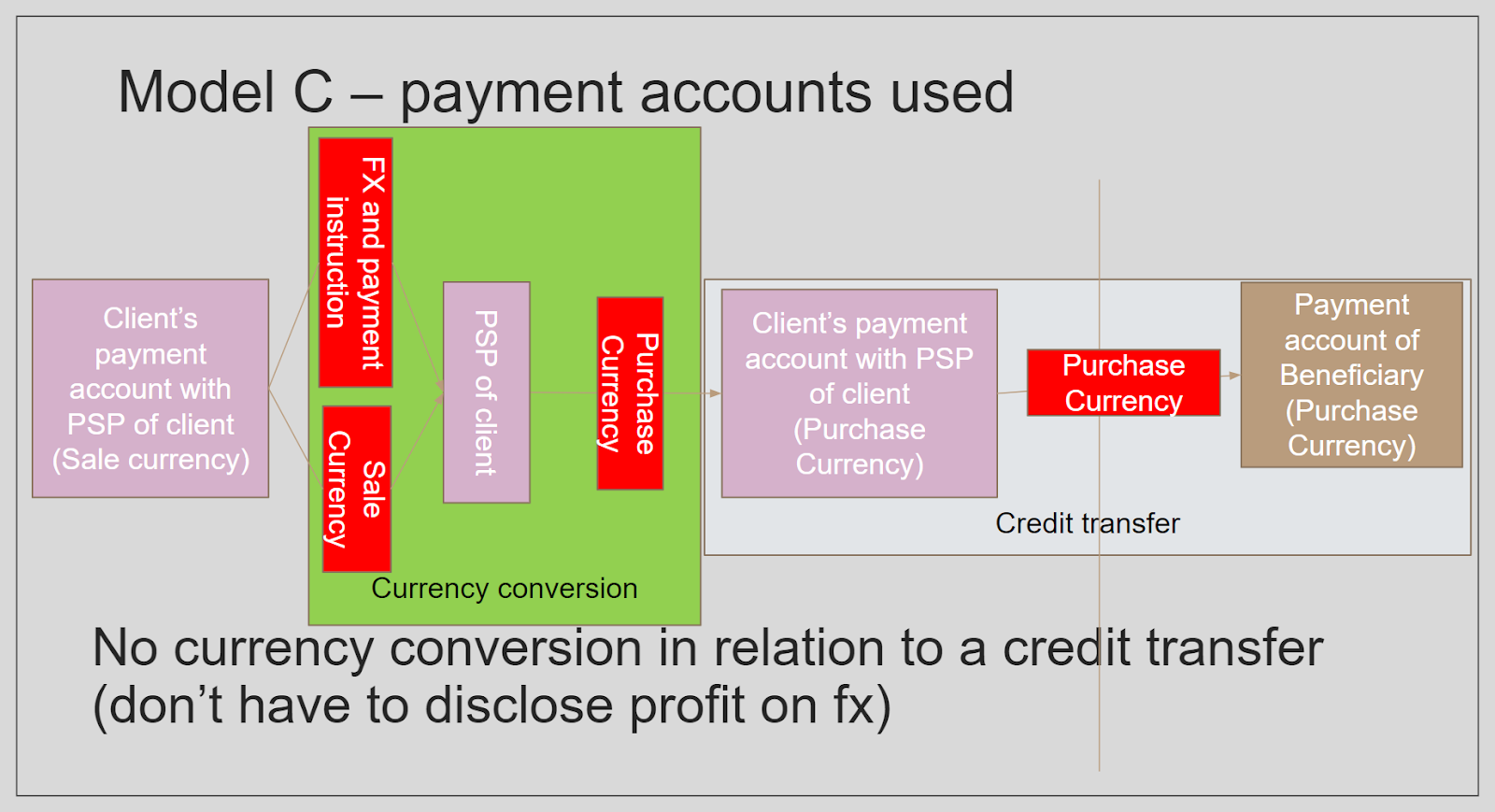

Model C

The final model I examine does have credit transfer and does have currency conversion, but in our view the currency conversion is not in relation to the credit transfer. Instead, it happens before the transfer.

Article 3b does not apply here.

Summing up

Here are some summary points:

- if you don’t offer payment accounts (including electronic money accounts), but simply offer money remittance, then Article 3b does not apply;

- if you do offer payment accounts (including electronic money accounts), then you must ensure that you credit the purchase monies from the currency conversion to a payment account in the purchase currency prior to executing the credit transfer. There will then be no currency conversion in relation to the credit transfer;

- if you are using model c, ensure that you have a payment account for all the purchase currencies you are offering;

- make sure your terms & conditions reflect your practice in relation to your funds flow model, i.e. if you are using model c, state that the payment account in the purchase currency is credited prior to credit transfer; and

- make sure you have a written internal note, legal opinion or other form of justification document on your file that sets out why you are not obliged to comply with Article 3b.

Has the FCA Granted Any Concessions for COVID19?

The Financial Conduct Authority issued a statement after the video was recorded. It can be found on their website under Cross-border payments regulation.

In their statement, the FCA makes clear that it expects firms to comply with the transparency requirements where they can. However, the FCA will take a ‘reasonable approach’ towards rule enforcement in light of the need to preserve the stability and continuity of online payment services. This may mean assessing the immediate need to meet the new transparency obligations against the risk of introducing non-essential risk or a significant reduction in a firm’s capacity to deliver frontline services to customers.

To watch my webinar, see the video below.

Let’s Talk

If you have any specific questions about CBPR2, or would like further advice please contact us .

Contact Creed Solicitors for legal advice on whether CBRP2 applies to your foreign exchange and payment company or any other legal payments queries.

Photo by Martin Krchnacek on Unsplash